Did you think central bankers are out of bullets? They are just getting started!

A couple of years ago, during the immediate aftermath of the financial crisis, central banks rolled out a bundle of monetary measures, considered to be unorthodox at the time. Liquidity injections, swaps, asset purchasing programmes, and later negative interest rates and asymmetric interest rate corridors were all in the magazine. These policies seemingly reached their limit, yet leading central banks are still struggling to generate wage growth and substantial inflation throughout the global economy.

For the last more than half a century there has been a status quo regarding the correlation between the two factors. However, new times require new paradigms. The theoretical foundation of contemporary monetary policy is called the ‘Phillips-curve‘. Besides that the original theory was formed around the UK labour market in the 1950s, describing a non-globalised, manufacturing heavy, technologically limited Western economy, policymakers often miss other flaws of the model. Even from a technical perspective, the model does not suggest the necessity of increasing inflation as a consequence of tight labour market. The function also accounts for inflation expectations, and external shocks (meaning: changes not in the inflationary or labour environment). After 30+ years of decelerating inflation, opening of economic borders, structural changes in the economies, and shifting demographics it would be hard to argue that tight labour market (which, by the way, is only relying on a single metric of headline unemployment) is the single most significant factor in inflation generation. However, one must give credit to the fact that in lower competition for job openings workers’ negotiating power certainly increases.

Enacting loose monetary policy, central bankers around the world could stop the bleeding by pumping enormous amount of liquidity on the markets, thus lubricating financial transactions. The result is ultra cheap money, high valuations, and capital cost optimisation through corporate leveraging. They were able to keep the enterprises and workplaces afloat, even though negative side-effects arose, such as the deteriorating marginal efficiency of wealth effect, or the emergence of a zombie sectors, whose debt-servicing capabilities rely on ultra low yields.

The next stage is going to be a bit more complicated. As I mentioned above, wage growth is still missing, while asset prices are soaring. This is especially troubling for some millennials who trying to get their first home and have to save up for the deposit. Some central banks – sensing that they have reached the limit of orthodox unorthodoxy – surpass their mandate, and deploy a brand new policy tool: make direct recommendations to the public instead of nudging them by setting financial conditions. The Reserve Bank of Australia urges employees to negotiate for higher wages. However, in a globalised marketplace with no inflation, and cheap financing for automation, it is hard to nudge the labour market to negotiate for higher nominal wages. As every policy tool, this measure can be used as a two-edged sword as well. In Indonesia, deputy governor Rosmaya Hadi asked religious leaders to preach against lavish spending, trying to curb inflation numbers.

The gridlock of inflation

Paradoxically, generating inflation, alias accelerating it, would be easier if we had some currency depreciation in the first place. Somewhat, but meaningfully positive nominal rates would make debt-servicing costly for zombie companies, provide cash flow for fixed income investors, and help banks to recapitalise to start lending again; all without putting real interest burden on the economy. These are just a couple of reasons why economists argue for higher inflation targets. However, it is not an easy job to convince the generation of central bankers, who grew up in a double digit inflationary environment, to change their mindset about higher targets.

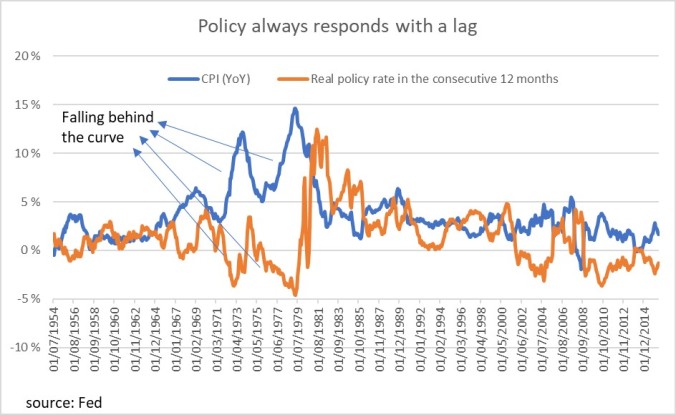

Just as generals always try to win the last war, central bankers always try to respond to the last crisis. This contributed to the high inflation in the 1970s, when policymaker – remembering the deflationary pressure in the 1930s – fell behind the curve and let real policy rate go well below zero (see graph). Nowadays, when the memory of taming inflation is still vivid, the challenge won’t be coming up with newer policy measures to make someone else do the job. It will be to turn back to ‘ye olde’ monetary tools and raise the inflation target. That will be the unorthodox game changer.